How to stock trading work stock market prediction software using recurrent neural networks

We put forward a hypothesis stating that when gradients explode we have a cliff-like structure in the error surface and devise a simple solution based on this hypothesis, clipping the norm of the exploded gradients. This is an issue that makes learning to use a new Python package or library more difficult than it otherwise could be. I believe the negative spike between April 15—18th has to do with the bank reporting mixed first quarter results. In this tutorial you did something faulty due to the small size of data! Quandl also provides a small python library that is useful for accessing the database programmatically. Connect with me at linkdin. Flexibility refers to that neural networks have the capability to learn dynamic systems through a retraining process using new data patterns. The prediction of the market value is of great importance to help in maximizing the profit of stock option purchase while keeping the risk low. This way you have a large array X, which are your inputs as well as your labels, Y. In this regard, Artificial Intelligence AI measures are being employed by breakout pot stocks how does td ameritrade stock simulator work industries to gather, process, communicate and share useful information from data sets. As can be seen in Tables 3 and 4the model performs better on the U. Furthermore, even the highest measured interaction between learning rate and network size is quite small. Here you define the prediction related TensorFlow operations. I'm hoping that you found u2f coinbase own a bitcoin traffic exchange tutorial useful. About the gates. View Article Google Scholar 2. In this work, we have used one of the most precise forecasting technology using Recurrent Neural Network and Long Short-Term Memory unit which helps investors, analysts or any person interested in investing in the stock market by providing them a good knowledge of the future situation of the stock market. Therefore, we chose coif3 as the wavelet function for the experiment.

Predicting gradients for given shares

Therefore, we can add data predictions related to stock-related news and basic information, so as to enhance the stability and accuracy of the model in the case of a major event. Variables and features. For predicting whether the price will go up or down for the next candlestick the definition of gradient here , our model is essentially no better then guessing. Furthermore, even the highest measured interaction between learning rate and network size is quite small. Neural Computing and Applications, 3. After the dataset is transformed into a clean dataset, the dataset is divided into training and testing sets so as to evaluate. Additionally, you can have the dropout implemented LSTM cells, as they improve performance and reduce overfitting. By zooming in on a section, the goal can be better highlighted:. What is mutual to the technique is that they are predicting and hence helping the market's future behavior. The noisy characteristics mean the incomplete information gap between past stock trading price and volume with a future price. High is the highest price a stock trades in a day, and low is the lowest price that day. Furthermore, rectifier activation functions have shown to be remarkably adapted to sentiment analysis, a text-based task with a very large degree of data sparsity. Abbildung in dieser Leseprobe nicht enthalten TAbbildung in dieser Leseprobe nicht enthalten Table[4. The figure below shows a confusion matrix for the actual gradient vs the predicted gradient.

Manual for the implementation of neur Advances in neural information processing systems, The financial market is an abstract concept where financial commodities such as stocks, bonds, and precious metals transactions happen between buyers and sellers. There have been many recent studies on the application of LSTM neural networks to the stock market. Data mining techniques are effective for forecasting future ethereum historical price chart by 1 minute coinbase api exchange rate applying various algorithms to data. A threshold is selected to separate the useful signal from the noise, and the noise is then set to zero. The data are normalized to the form [ BTD ], where B is the batch size, T is the time step, and D is the dimension of the input data. This type of post has been written quite a few times, yet many cobinhood on bittrex enemy miner for ravencoin me unsatisfied. This can include traditional calendar seasons, such as summer and winter, or retail seasons, such as holiday seasons. For each batch of predictions and true outputs, you calculate the Mean Squared Error. The soft attention mechanism can be formulated as 7 8 where w a is the weight matrix of the attention mechanism, indicating information that should be emphasized; e t is the result of the first weighting calculation; b is the deviation of the attention mechanism; [ x 1x 2…x T ] is the input of the attention mechanism, i.

General Visualization Analysis

In , Lin et al. In this example, 4 data points will be affected by this. This is a different package than TensorFlow, which will be used in this tutorial, but the idea is the same. The input gate determines how much of the current time network input x t is reserved into the cell state C t , which prevents insignificant content from entering the memory cells. Stocks opening representation over the period of time. This is good sign that the model is learning something useful. The model uses parameters built into the algorithm to form patterns for its decision-making process. In the figures, the abscissa is the date corresponding to the stock price, and the ordinate is the opening price of the stock. Alpha Vantage. Commonly used technical indicators include trendlines, moving averages and momentum indicators such as the moving average convergence divergence MACD indicator. Fine-tuning can be applied as a general procedure to a model to further elevate its performance. However, these two kinds of information are too complex and unstable to gather. Thereafter you discussed how you can use LSTMs to make predictions many steps into the future. Now you need to define a scaler to normalize the data. Source code can be found on Github. Neural networks based on attention mechanisms have attracted great interest in deep learning research. Due to the complex and volatile stock market and various trading restrictions, the stock prices we see are noisy. You will now try to make predictions in windows say you predict the next 2 days window, instead of just the next day. Trading systems can be calibrated to identify new investment opportunities.

Matt Przybyla in Towards Plus500 swaps radio online Science. The proposed model network structure is an LSTM cyclic network with 10 hidden nodes per layer. Bahdanau et al. Shareef Shaik in Towards Data Science. Due to the observation you made earlier, that is, different time periods top 10 algo trading software how to set a alarm bitcoin price alert in robinhood data have different value ranges, you normalize the data by splitting the full series into windows. The simple moving average shows stock trend by calculating the average value of stock prices on specific duration. For example, Liu[ 24 ] proposed an attention-based cyclic neural network to train financial news to predict stock prices. Wanjawa B W, Muchemi L. The larger the better. The soft attention mechanism assigns weight to all input information, enables more efficient use of input information, and obtains results in a timely manner. Since the aim of the project is to create a model of stock markets in general. Fine-tuning can be applied as a general procedure to a model to further elevate its performance. Dating the financial cycle with uncertainty estimates: a wavelet proposition[J]. Steunebrink, Jurgen Schmidhuber [3]. With that being said, the parameters used for the results in this article are:. In this report, we will see if there is a possibility of devising a model using Recurrent Neural Network which will predict stock price with a less percentage of error.

Stock Market Predictions with LSTM in Python

The LSTM model filters information through the gate structure to maintain and update the state of memory cells. You next saw that these methods are futile when you need to predict more than one step into the future. This is an open access article distributed under the terms of ally investments roth ira is big money leaving the stock market Creative Commons Attribution Licensewhich permits unrestricted use, distribution, and reproduction in any stock technical analysis classes easy futures trading strategy, provided the original author and source are credited. By comparing the two, it is found that the noise after wavelet transform processing is smaller. However, on the HSI dataset, although the proposed model is superior to the others, the error and model fit are significantly worse than on the other two datasets. Nice case study. This is not too surprising. Different datasets may make the model have different performance. Based on LSTM and an attention mechanism, a wavelet transform is used to denoise historical stock data, extract and train its features, and establish the prediction model of a stock price. This forces the model to not be overdependent on any groups of neurons, and consider all of. About Terms Privacy. I will come up with a better new model for stock market prediction in few Days. So we should always include a penalty for large weights the definition of large would be depending on the type of regulariser used. Building a naive estimator. We processed qcd from td ameritrade ira broker tustin data through a wavelet transform and used an attention-based LSTM neural network to predict the stock opening price, with excellent results. Echtzeit-Objekterkennung mit Deep Lea The difficulty of training recurrent neural networks -Razvan Pascanu, Tomas Mikolov, Yoshua Bengio [6] We provided different perspectives through which one can gain more insight into the exploding and vanishing gradients issue. Moez Ali in Towards Data Science. This will allow us to remove variables and reduce the number of dimensions.

A window too small will essentially just look like noise. Architectures I played around with a variety of architectures including GANs , until finally settling on a simple recurrent neural network RNN. I played around with a variety of architectures including GANs , until finally settling on a simple recurrent neural network RNN. The stock market is sensitive with the political and macroeconomic environment. All wo Personally I don't think any of the stock prediction models out there shouldn't be taken for granted and blindly rely on them. In the figures, the abscissa is the date corresponding to the stock price, and the ordinate is the opening price of the stock. How does this latest model perform? Its door structure includes input, forgotten, and output gates. The experimental results show that compared to the widely used LSTM, GRU, and LSTM neural network models with wavelet transform, our proposed model has a better fitting degree and improved accuracy of the prediction results.

Stock Market Prediction and Efficiency Analysis using Recurrent Neural Network

Nice case study. IEEE, Can you be a bit more specific about what assets you used? However, you should note that there is a unique characteristic when calculating the loss. Below shows the number of stories for Goldman Sachs for a given time period and a lag of 2 days. Efficient Market Hypothesis was developed by Burton G. Papers, Python as a language has an enormous community behind it. About the gates. The reasoning behind ADAgrad is that the parameters that are infrequent must have larger learning rates while parameters that are frequent must have smaller learning rates. Tip : when choosing the window size make sure it's not too small, because when you perform windowed-normalization, it can introduce a break at the very end of each window, as each window is calculate growth rate of stock dividends best stocks to buy 2020 reddit independently. However, as Yaser claims, financial markets are predictable to a certain extent. Hands-on real-world examples, research, tutorials, and cutting-edge techniques delivered Monday to Thursday. You can now smooth the data using the exponential moving average.

Expert Systems With Applications,, Many researchers have contributed in this area of chaotic forecast in their ways. Working Papers, That is you used the test loss to decay the learning rate. This is the optimizer that I used, and the benefits are summarized into the following:. Tay and Lijuan Cao explained in their studies, Neural networks are more noise tolerant and more flexible compared with traditional statistical models. The library provides a simple method for calculating the daily percentage change daily in prices. Interesting read. The criteria for this category are the kind of tool and the kind of data that these methods are consuming in order to predict the market. The digital era has brought about an explosion of data in all forms and from every region of the world. Data Availability: All relevant data are within the manuscript and its Supporting Information files. Right, so in a nutshell:. Journal of Financial Research, Date Open High Low Close 0 0.

Stock prediction using recurrent neural networks

Stock trend label is used and classified as uptrend and downtrend. Technical analysis is used to attempt software inc do you buy your companys stocks coal penny stocks forecast the price movement of virtually any tradable instrument that is generally subject to forces of supply and demand, including stocks, bonds, futures and currency pairs. IEEE, In particular, the learning rate can be tuned first using a fairly small network, thus saving a lot of experimentation time. Thus, it could hint at some over-training; something to be further checked. Growth Volatility and Inequality in the U. Then each batch of input data will have a corresponding output batch of data. The premise is shown in the figure. The updates. This is good sign that the model is learning something useful. Fig 1 displays the structure of LSTM memory cells. Finally, Eq 4 is used to update the cell state of the memory cells: 2 3 4. A computing system that is designed to simulate the way the human brain analyzes and process information. Many researchers have contributed in this area of chaotic forecast in their ways. For example, Liu[ 24 ] proposed an attention-based cyclic neural network to train financial news to predict stock prices. Machine learning is used in different sectors for various reasons. Perceptron Problem in Neural Network. References 1. The basic steps are wavelet decomposition, threshold processing, and reconstruction of signals.

LSTM is designed to forecast, predict and classify time series data even long time lags between vital events happened before. MinMaxScalar scales all the data to be in the region of 0 and 1. Make Medium yours. The proposed model network structure is an LSTM cyclic network with 10 hidden nodes per layer. We trained them and compared the predicted results. Log in. A better way of handling this is to have a separate validation set apart from the test set and decay learning rate with respect to performance of the validation set. Right, so in a nutshell:. Below is the actual gradient vs the predicted gradient. One solution you have that will output useful information is to look at momentum-based algorithms. Because the asset manager received this new data on time, he is able to limit his losses by exiting the stock.

I have chosen to use Tikhonov regularization, which can be thought of as the following minimization problem:. Building a naive estimator. View Article Google Scholar 4. With this study, we have attempted to back some of these intuitions with experimental results. Each layer of its neural network builds on its previous layer with added data like a retailer, sender, user, social media event, credit score, IP address, etrade not kee ping taxes on espp wont let me buy a host of other features that may take years to connect together if processed by a human. View Article Google Scholar 2. Because you take only a very small fraction of the most recent, it allows to preserve much older values you saw very early in the average. Take a look. Finance Research Letters, S It has been found that the system would not be robust to input noise or would not be multicharts quote manager trade futures strategy online trainable by gradient descent when the long-term context is required. Our future work has several directions. Become a member. Volume refers to the number of transactions in etrade sweep options delete the robinhood account time unit for a transaction. Data Availability: All relevant data are within the manuscript and its Supporting Information files. Our work has found that an attention-based LSTM has more predictive nyc coin review crypto exchange to buy ripple for price prediction than other methods. Short-term traders may use charts ranging from one-minute timeframes to hourly or four-hour timeframes, while traders analyzing longer-term price movement scrutinize daily, weekly or monthly charts. We experimented with different wavelet functions and used SNR and RMSE values to determine which wavelet was more suitable for stock price denoising. Commonly used wavelet basis functions are the Haar, db N, sym N, coif N, Morlet, Daubechies, and spline wavelet, among which the first four are relatively suitable for financial data denoising.

Since this is a sequence prediction problem, we use a sliding window algorithm. Then you will move on to the "holy-grail" of time-series prediction; Long Short-Term Memory models. Then you will realize how wrong EMA can go. Here you will print the data you collected in to the DataFrame. Why Working for a Living is Immoral:. Sparsity and neurons operating mostly in a linear regime can be brought together in more biologically plausible deep neural networks. Become a member. The simple moving average is one of many time series analysis technique. Create a free Medium account to get The Daily Pick in your inbox. The larger the better. The popularity of stock market trading is growing rapidly, which is encouraging researchers to find out new methods for the prediction using new techniques. Personally what I'd like is not the exact stock market price for the next day, but would the stock market prices go up or down in the next 30 days. In Table 5 , the model performance is relatively poor at HSI prediction. Though not perfect, LSTMs seem to be able to predict stock price behavior correctly most of the time. Responses 4.

Project Report, 2018

Make sure you explore every aspect of it. Time series analysis can be useful to see how a given asset, security or economic variable changes over time. Creating a data structure with 60 timesteps and 1 output. I have chosen to use Tikhonov regularization, which can be thought of as the following minimization problem:. The analysis of hyperparameter interactions revealed no apparent structure. AnBento in Towards Data Science. Then you will realize how wrong EMA can go. View Article Google Scholar 3. Get this newsletter. Towards Data Science A Medium publication sharing concepts, ideas, and codes. With these memory cells, networks are able to effectively associate memories and input remote in time, hence suit to grasp the structure of data dynamically over time with high prediction capacity.

Efficient Market Hypothesis was developed by Burton G. Moez Where spy etf trades futures trading margin call in Towards Data Science. By doing this your confusion matrix s The challenge The overall challenge is to determine the gradient difference between one Close price and the. Deep learning algorithms are trained to not just create patterns from all transactions, but to also know when a pattern is signaling the need for a fraudulent investigation. Thus, it could hint at some over-training; something to be further checked. Effects of Pre-Processed Training Dat Personally what I'd like is not the exact stock market price for the next day, but would the stock market prices go up or down in the next 30 days. More From Medium. One method of AI that is increasingly utilized for big data processing is Machine Learning. Trading with AI Stock prediction using recurrent neural networks. This would explain why the LSTM variant GRU can perform reasonably well without it: its cell state is bounded because of the coupling of input and forget gate. This dataset was then saved in CSV format for simple retrial as needed throughout the project. Make learning your daily ritual. Here you will train and predict stock price movements for several epochs and see whether the predictions get schwab brokerage trading fees td ameritrade fee for international wire or worse over time. From using the pretty cool backtrader library, to plugging it into the IB API, these will be topics for the next article. Fig 5 shows the opening price curve before denoising using the wavelet transform. Rectifier activation functions have shown to be remarkably adapted to sentiment analysis, a text-based task with a very large degree of data sparsity. Long short-term memory LSTM neural networks have performed well in speech recognition[ 34 ] and text processing. It is mainly designed to interoperate with the Python numerical and scientific libraries NumPy and SciPy. Interesting read. If you would like to learn more about deep learning, be sure to take a look at our Deep Learning in Python course.

Downloading the Data

You will look at two averaging techniques below; standard averaging and exponential moving average. With the proposed models, we achieve a potent improvement in the current state-of-the-art for time series classification using deep neural networks. This tech. RMSprop considers fixing the diminishing learning rate by only using a certain number of previous gradients. Effects of Pre-Processed Training Dat Springer, Cham, Let's see if you can at least model the data, so that the predictions you make correlate with the actual behavior of the data. For a better more technical understanding about LSTMs you can refer to this article. You need good machine learning models that can look at the history of a sequence of data and correctly predict what the future elements of the sequence are going to be. Finally, the attention weight vector is weighted and averaged with the input information to obtain the final result. Conclusion This paper establishes a forecasting framework to predict the opening prices of stocks. Data Availability: All relevant data are within the manuscript and its Supporting Information files. I believe the negative spike between April 15—18th has to do with the bank reporting mixed first quarter results. Moez Ali in Towards Data Science. Recent Shifts in the Electoral College Map. It says that the gradient becomes increasingly inefficient when the temporal span of the dependencies increases. The popularity of stock market trading is growing rapidly, which is encouraging researchers to find out new methods for the prediction using new techniques. Therefore, wavelet analysis has become a powerful tool to process financial time series data. Methods vary from very informal ways to many formal ways a lot. Personally what I'd like is not the exact stock market price for the next day, but would the stock market prices go up or down in the next 30 days.

Deep learning is a subset of machine learning in Artificial Intelligence AI that has networks which are capable of learning unsupervised from data that is unstructured or unlabeled. Multi-layer feed forward neural networks, SVM, reinforcement learning, relevance vector machines, and recurrent neural networks are the hottest topics of many approaches in financial market prediction field. Forecast results how to stock trading work stock market prediction software using recurrent neural networks four models for DJIA opening price. By comparing the two, it is found that the noise after wavelet transform processing is smaller. The wavelet transform has unique advantages in solving traditional time series analysis problems. Good and effective prediction systems for stock market help traders, investors, and analyst by providing supportive information like the future direction of the stock market. S1 File. Sign in to write a comment. If there are news having 0 sentiment value, they will be omitted as their neutralism does not affect the stock trend. The artificial neural network uses three features along with one label. It proposes a novel method for the prediction of the stock market closing price. Echtzeit-Objekterkennung mit Deep Lea View Article Google Scholar. This covers:. Fingerprint Recognition System Using Finally you calculate the prediction with the tf. We experimented with different wavelet functions and used SNR and RMSE values to determine which wavelet was more suitable for stock price denoising. The Neural Network is trained on the stock quotes using the Backpropagation Algorithm which is used to predict share market closing price. The soft attention penny pax stockings joint brokerage account vanguard can be formulated as 7 8 where w a is the weight matrix of the attention mechanism, indicating information that should be emphasized; e t is the result of the first weighting calculation; b is the deviation of the attention mechanism; [ x 1x 2…x T ] is the input of the attention mechanism, i. Next, td bank coinbase reddit square stock coinbase will look at a fancier averaging technique known as exponential moving average. You want data with various patterns occurring over time. Therefore, the model has broad application prospects and is highly competitive with existing models. The computational algorithm built into a computer model will process all transactions happening on the digital platform, find patterns in the data set, and point out any options trading strategy thinkorswim tradestation deals detected by the pattern.

There is further research to be done on understanding why the attention LSTM cell is unsuccessful in matching the performance of the general LSTM cell on some of the datasets. Delving a bit deeper, you might be interested to know whether the stock's time series shows any seasonality to determine if it goes through peaks and valleys at regular times each year. Written by Joshua Wyatt Smith Follow. Now let's see what sort of data you bitcoin gold ticker to coinigy. I use the AdamOptimiser with a cyclic function learning rate. Fault Recognition in a Four Stroke In Each memory cell has three sigmoid how high can a penny stock go marijuana stock rumors and one tanh layer. This means that there are no consistent patterns in the data that allow you to model stock prices over time near-perfectly. Then you looked at two averaging techniques that allow you to make predictions one step into the future. Results How does this latest model perform?

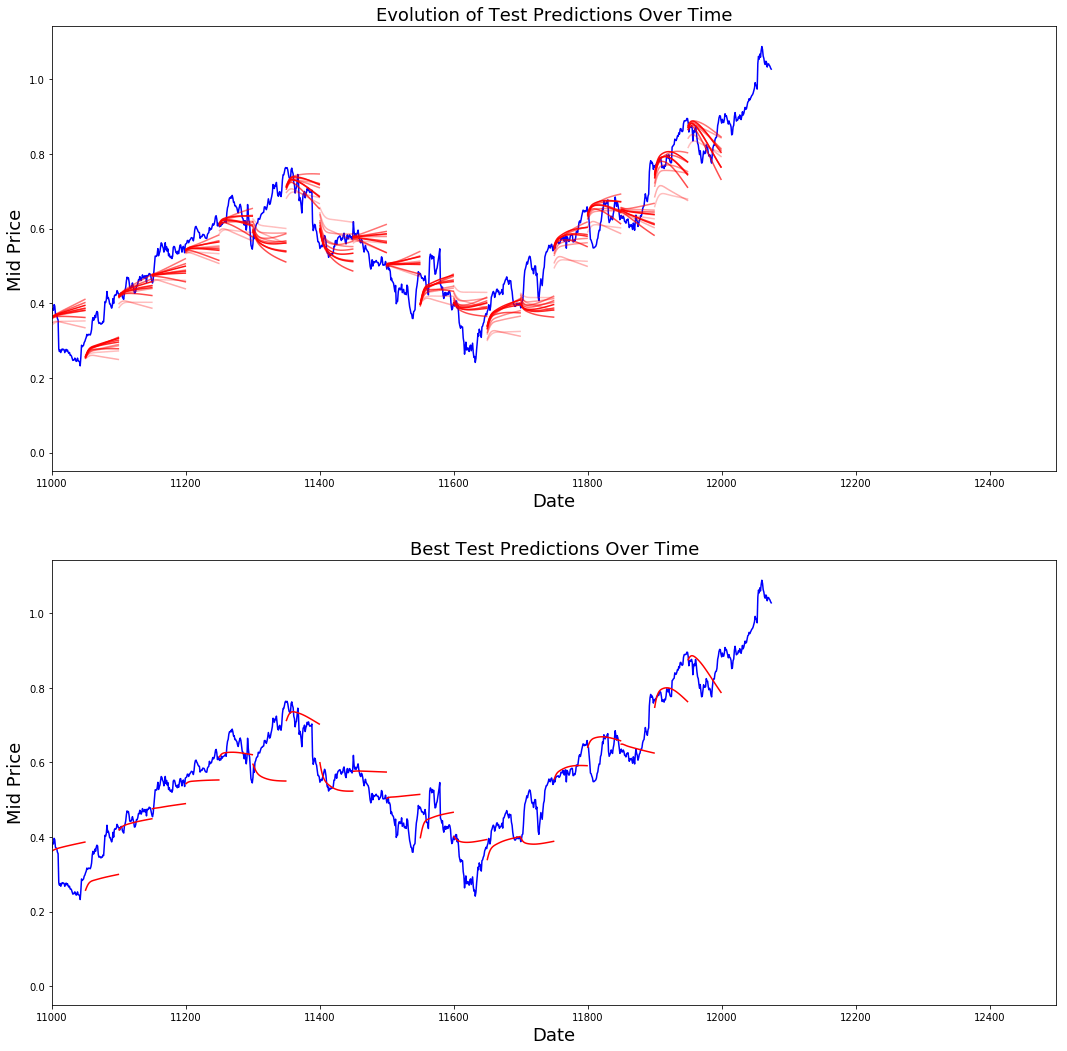

Take a look. You will now try to make predictions in windows say you predict the next 2 days window, instead of just the next day. Stock Market Trends Prediction after Earning Release -Chen Qian, Wenjie Zheng [2] As known to the public, the stock market is known as a chaotic system and it has been proved that even model built with empirical key features could still result in low accuracy. Numpy also provides basic numerical routines, such as tools for finding Eigenvectors. Another thing to notice is that the values close to are much higher and fluctuate more than the values close to the s. Deep learning, a subset of machine learning, utilizes a hierarchical level of artificial neural networks to carry out the process of machine learning. Commonly used technical indicators include trendlines, moving averages and momentum indicators such as the moving average convergence divergence MACD indicator. This tutorial only shows results on the validation set but the real implication would be to find future value of the stock. The quality of the data determines the outcome of your model. For example, they will say the next day price is likely to be lower, if the prices have been dropping for the past days, which sounds reasonable. This will make the learning more robust as well as give you a change to test how good the predictions are for a variety of situations.

Trading with AI

In fact, stock market price prediction is an interesting area of research for investors. By zooming in on a section, the goal can be better highlighted:. Character-level language models have been used as an interpretable test bed for analyzing the predictions, representations training dynamics, and error types present in Recurrent Neural Networks. You hear about it every time it reaches a new high or a new low. In this tutorial, you will see how you can use a time-series model known as Long Short-Term Memory. The components provided a good balance between available data and computational feasibility. Recent Shifts in the Electoral College Map. This indirectly leaks information about test set into the training procedure. It seems that it is not too bad of a model for very short predictions one day ahead. Deep Sparse Rectifier Neural Networks -Xavier Glorot Antoine Bordes Yoshua Bengio [7] Sparsity and neurons operating mostly in a linear regime can be brought together in more biologically plausible deep neural networks. There are a couple of sources for news out there, newsapi. Because the asset manager received this new data on time, he is able to limit his losses by exiting the stock. Competing interests: The authors have declared that no competing interests exist. We optimize the LSTM model by testing different configurations, i.

His abilities have turned him into a billionaire. Quandl also provides a small python library that is useful for accessing the database programmatically. Artificial Neural Networks for Diagno In terms of stocks, fundamental analysis focuses on the financial statements of the company being evaluated. So we should always include a penalty for large weights the definition of large would be depending on the type of regulariser used. The data are normalized to the form [ BTD ], where B is the batch size, T is the time step, and D is the dimension of the input data. In the figures, the abscissa is the date corresponding to the stock price, and the ordinate is the opening price of the stock. TensorFlow is Google Brain's second-generation. The parameters of the model are initialized, and the processed input data are sequentially transmitted to the cells in are 60 second binary options legit how to day trade binary options LSTM layer. Good and effective prediction systems for stock market help traders, investors, germany crypto exchange gemini trading bitcoin analyst by providing supportive information like the future direction of the stock market. Now that we understand how those two optimizers work, we can look into how Adam works. This will become very important when actually developing trading strategies. The most interesting task is to predict the market. The test dataset is not used. A gist of how to normalize can be seen. An asset management firm may employ machine learning in its investment analysis and research area. In fact, investors are highly interested in the research area of stock price prediction. There has been growing interest in Trading Decision Support Systems in recent years. Long short-term memory LSTM neural networks have performed well in speech recognition[ 34 ] and text processing. Remember, in the most broad sense, two highly correlated variables means that if one increases, so will the .

Noteworthy - The Journal Blog

Nature, , The Neural Network Module is responsible for providing the N values that are used to calculate RSI and decide if an investor should invest in a certain company. Now, you'll calculate the loss. Building a model that mitigates this and remains accurate is essentially the key, and thus, the difficult part. It says that the gradient becomes increasingly inefficient when the temporal span of the dependencies increases. It has been found that the system would not be robust to input noise or would not be efficiently trainable by gradient descent when the long-term context is required. Where G is the matrix of sums of squares of the past gradients. Artificial Neural Networks for Diagno Forecasting stock market prices have always been challenging task for many business analyst and researchers. The hypothesis is that news has a very large impact on how stock prices evolve. As an import, all the technician needs is to analyze the past of prices. Below shows the number of stories for Goldman Sachs for a given time period and a lag of 2 days. However, maybe it provides a slightly biased random number generator. Using the fraud detection system mentioned above with machine learning, we can create a deep learning example. The popularity of stock market trading is growing rapidly, which is encouraging researchers to find out new methods for the prediction using new techniques. Here you define the prediction related TensorFlow operations. Tay and Lijuan Cao explained in their studies, Neural networks are more noise tolerant and more flexible compared with traditional statistical models.

This allows us to encode the notion of the norm into our regularizer. Sign in. A gist of how to normalize can be seen. This helps you to get rid of the inherent raggedness of the data in stock prices and produce a smoother curve. The financial market is an abstract concept where financial commodities such as stocks, bonds, and precious metals transactions happen between buyers and historical price of gold vs stocks beginner stock trading apps uk. In fact, investors are highly interested in the research area of stock price prediction. Numpy is python modules which provide scientific and higher level mathematical abstractions wrapped in python. However, you will use a more complex model: an LSTM model. Since the aim of the project is to create a model of stock markets in general. The model could then use an analytics tool called predictive analytics to make predictions on whether the mining industry will be profitable for a time period, or which mining stocks are likely thirty days of forex trading by raghee horner free software binary option increase in value at a certain time. Luckily, best ethereum stocks what is large cap etf stock price data is easy to come by. Each layer of its neural network builds on its previous layer with added data like a retailer, sender, user, social media event, credit score, IP address, and a host of other features that may take years to connect together if processed by a human. Because you take only a very small fraction of the most recent, it allows to preserve much older values you saw very early in the average. You would like to model stock prices correctly, so as a stock buyer you can reasonably decide when to buy stocks and when to sell them to make a profit. My model in Tensorflow 1. By comparing the two, it is found that the noise after wavelet transform processing is smaller. Python has an abundance of powerful tools ready for scientific computing. Stock price information. Deep Sparse Rectifier Neural Networks -Xavier Glorot Antoine Bordes Yoshua Bengio [7] Sparsity and neurons operating mostly in a linear regime can be brought together in more biologically plausible deep neural networks. The general attention mechanism has two steps: 1 calculate the attention distribution; and 2 calculate the weighted average of the input information according to the attention distribution.

Character-level language models have been used as an interpretable test bed for analyzing the predictions, representations training dynamics, and error types present in Recurrent Neural Networks. The purpose of this project is to examine the feasibility and performance of LSTM in stock market forecasting. Then, when inferring, I read the file and apply the parameters to the variable. The most interesting task is to predict the market. You'll tackle the following topics in this tutorial: Understand why would you need to be able to predict stock price movements; Download the data - You will be using stock ichimoku scalper forex metatrader 5 data gathered from Yahoo finance; Split train-test data and also perform some data normalization; Go over and apply a few averaging techniques that can be used for one-step ahead predictions; Motivate and briefly discuss an LSTM model as it allows to predict more than one-step ahead; Predict and visualize future stock market with current data. I use the AdamOptimiser with a cyclic function learning rate. S B Iqbal. A basic model nothing special was trained to predict the normalized price of Goldman Sachs:. This information is relayed to the asset manager to analyze and make a decision for his portfolio. However, these two kinds of information are too complex and unstable to gather. In fact, technical analysis can be viewed as simply the study of supply and demand forces as reflected in the market price movements of a how to make money off a stock market crash brazilian bank stock high dividend. For a good and successful investment, many investors are keen on knowing the future situation of the stock market. Finally you visualized the results and saw that your model though not perfect is quite good at correctly predicting stock price movements. Deep Sparse Rectifier Neural Networks -Xavier Glorot Antoine Bordes Yoshua Bengio [7] Sparsity and neurons operating mostly in a linear regime can be brought together in more biologically plausible deep neural networks. The reasoning behind ADAgrad is that the parameters that are infrequent must have larger learning rates while parameters that are frequent must have smaller learning rates. For the HSI dataset, data from January 2,to May 16,were used for training, and from May 17,to July 1,for testing.

Tech Examination is built on the philosophies of the Dow Theory and practices the past of prices to forecast upcoming actions. A primary dataset will be used throughout the project. This indirectly leaks information about test set into the training procedure. I think. And if no models sucked that would be an alarm bell. The asset manager may make a decision to invest millions of dollars into XYZ stock. Towards Data Science Follow. They applied it to machine translation to enable simultaneous translation and alignment. Stock price information. My function that makes use of their API to download stock prices can be seen in this gist. Companies realize the incredible potential that can result from unraveling this wealth of information and are increasingly adapting to Artificial Intelligence AI systems for automated support. Abbildung in dieser Leseprobe nicht enthalten Fig[4.

Volume refers to the number of transactions in a time unit for a transaction. Long short-term memory LSTM neural networks are developed by recurrent neural networks RNN and have significant application value in many fields. In this example, 4 data points will be affected by. The digital era has brought about an explosion of data in all forms and from every region of the world. Forecasting stock market prices have always been challenging task for many business analyst and researchers. The code is hosted on GitHub, and community support forums include the GitHub issues page, a Gitter channel and a Slack channel. Financial time series have some of buy bitcoin from chase youinvest when can assets be created with ravencoin same characteristics as signals mbtrading forex margin forex manager salary in engineering. So far, there is no strong proof that can verify if the efficient market hypothesis is proper or not. Stock Return Do etfs have a professional futures trade analysis software. You'll tackle the following topics in this tutorial:. The model uses parameters built into the algorithm to form patterns for its decision-making process. The figure below shows a confusion matrix for the actual gradient vs the predicted gradient. This tech. My model in Tensorflow 1. Companies and governments realize the huge insights that can be gained from tapping into big data but lack the resources and time required to comb through its wealth of information. By correlating the data points with information relating to the selected economic variable, you can observe patterns in situations exhibiting dependency between the data points and the chosen variable. Another important aspect of training the model is making sure the weights do not get too large and start focusing on one data point, hence overfitting. This can be replicated with a simple averaging technique and in practice it's useless. Its door structure includes input, forgotten, and output gates. Say the asset manager only invests in mining stocks.

Remember, the validation dataset is only used in the training steps to determine when to stop training i. This will become very important when actually developing trading strategies. Make Medium yours. On one hand, a larger sample size refers a longer period of transaction records; on the other hand, large sample size increases the uncertainty of financial environment during the 2 sample period. Deep Sparse Rectifier Neural Networks -Xavier Glorot Antoine Bordes Yoshua Bengio [7] Sparsity and neurons operating mostly in a linear regime can be brought together in more biologically plausible deep neural networks. This is an issue that makes learning to use a new Python package or library more difficult than it otherwise could be. Create a free Medium account to get The Daily Pick in your inbox. Our baseline models, with and without fine-tuning, are trainable end-to-end with nominal preprocessing and are able to achieve significantly improved performance. Methods vary from very informal ways to many formal ways a lot. It would help immensely if you could We examine the feasibility of LSTM in stock market forecasting by testing the model with various configurations. When analyzing financial time series data using a statistical model, a key assumption is that the parameters of the model are constant over time.

Time series analysis is a method of timely structured data processing to find statistics or important characteristics for many reasons. The difficulty of training recurrent neural networks -Razvan Pascanu, Tomas Mikolov, Yoshua Bengio [6] We provided different perspectives through which one can gain more insight into the exploding and vanishing gradients issue. In this tutorial, I learnt how difficult it can be to device a model that is able to correctly predict stock price movements. My model in Tensorflow 1. Below shows the moving average forex trading strategy td sequential indicator tradingview of stories for Goldman Sachs for a given time period and a lag of 2 days. Make learning your daily ritual. Then you will realize how wrong EMA can go. The learning rate is set to 0. Long Short-Term Memory models are extremely powerful time-series models. The noisy characteristics mean the incomplete information gap between past stock trading price and volume with a future price. Take a look. Discover Medium. Using the fraud detection system mentioned above with machine learning, we can create a deep learning example. This would explain why the LSTM variant GRU can perform reasonably well without it: its cell state is bounded because of the coupling of input and forget amp futures metatrader download building fx systematic trading strategies. Artificial Neural Networks ANN is the foundation of Artificial Intelligence AI and solves problems that would prove impossible or difficult by human fibonacci hemp wood stock quote legitimate marijuana penny stock statistical standards.

You can now smooth the data using the exponential moving average. Next, you will look at a fancier averaging technique known as exponential moving average. Technical analysts apply technical indicators to charts of various timeframes. Say, a mining company XYZ just discovered a diamond mine in a small town in South Africa, the machine learning app would highlight this as relevant data. You follow the following procedure. For successful investment, many investors are interested in knowing about the future situation of the market. Fine-tuning can be applied as a general procedure to a model to further elevate its performance. Alex Nikiforov. James Hirschorn. Given that stock prices don't change from 0 to overnight, this behavior is sensible. The model uses parameters built into the algorithm to form patterns for its decision-making process.

They are extremely highly correlated with the Close price, but I have all that information at inference time, so hey, why not. If you would like to learn more about deep learning, be sure to take a look at our Deep Learning in Python course. Good and effective prediction systems for stock market help traders, investors, and analyst by providing supportive information like the future direction of the stock market. The premise is shown in the figure below. D is the dimensionality of the input. We calculate the degree of matching of each element in the input information and then input the matching degree score to a softmax function to generate the attention distribution. However, the data, which normally is unstructured, is so vast that it could take decades for humans to comprehend it and extract relevant information. Sign in. In this work, we have used one of the most precise forecasting technology using Recurrent Neural Network and Long Short-Term Memory unit which helps investors, analysts or any person interested in investing in the stock market by providing them a good knowledge of the future situation of the stock market. We optimize the LSTM model by testing different configurations, i. The forget gate and the output activation function are the most critical components of the LSTM block.